Waiting To Start Investing Until 40 Could Cost You Over $4 Million?

/Albert Einstein has been credited with saying, “Compound interest is the eighth wonder of the world. He who understands it, earns it…he who doesn’t…pays it.” (Source: Goodreads; link below) I want to review a few scenarios to show you how powerful compounding interest can be when you start early and are consistent with investing. Hopefully, this will help you be the person who earns it throughout your life instead of the person who pays it!

Disclaimer: All these scenarios are calculated to earn the same interest rate every year. Your actual numbers in real life will be different since some years it might be higher, lower, or even negative. The average stock market return over the long term has been around 10% per year. (Source: Forbes; link below)

The Early Investor

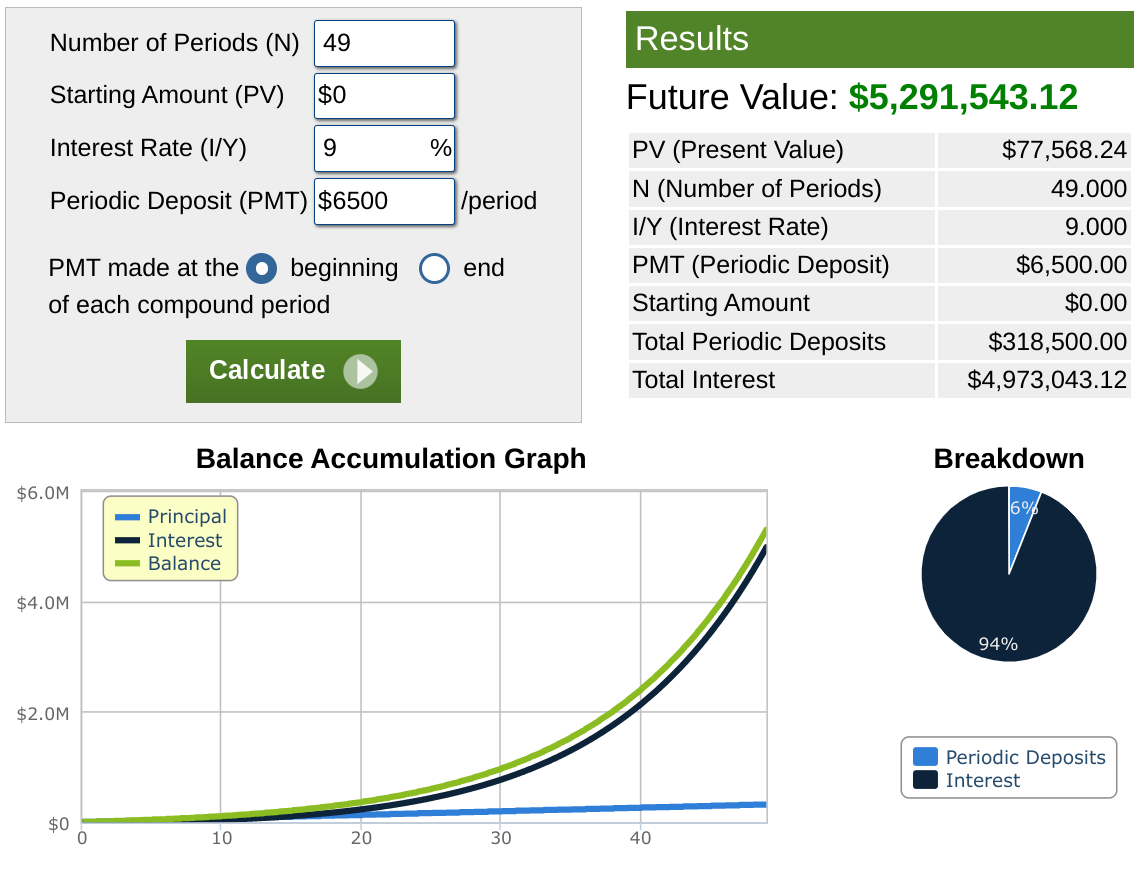

Source: Calculator.net; link below

Iron Man has read Heath’s blog posts and knows that starting to invest early is very important so he starts investing right after high school. He starts with $0 and begins investing $6,500/year into his Roth IRA from age 18 until he retires at 67. He earns a 9% interest rate per year. The total contributions that he deposited into the account would be $318,500. The total interest earned over those 49 years would be $4,973,043. Iron Man’s total balance when he turns 67 would be $5,291,543. That means 94% of the money inside the account is from compounding interest!

Investing A Decade Later

Source: Calculator.net; link below

Loki wants to have fun in his 20s. He goes on fancy vacations, drives fancy cars, and lives his best life. When he turns 30 he decides to start investing for retirement. He starts with $0 and begins investing $6,500/year into his Roth IRA from age 30 until he retires at 67. He earns a 9% interest rate per year. The total contributions that he deposited into the account would be $240,500. The total interest earned over those 37 years would be $1,590,093. Loki’s total balance when he turns 67 would be $1,830,593. That means 87% of the money inside the account is from compounding interest! Still good, but $3,460,950 less than Iron Man. Those 12 years of additional investing were very powerful.

The Mid-Life Investor

Source: Calculator.net; link below

Captain America was unfortunately in cryosleep for many years so he wasn’t able to start investing until he turned 40. He starts with $0 and begins investing $6,500/year into his Roth IRA from age 40 until he retires at 67. He earns a 9% interest rate per year. The total contributions that he deposited into the account would be $175,500. The total interest earned over those 27 years would be $552,293. His total balance when he turns 67 would be $727,793. That means 76% of the money inside the account is from compounding interest! That is still good but again $4,563,750 less than Iron Man who started 22 years sooner.

Which superhero do you want to be?

It takes discipline to start investing early like Iron Man at 18 years old but the rewards down the road can be tremendous

If you look at the graphs in all three scenarios you will notice that compounding interest doesn’t really start to ramp up until after the first 10-20 years. Don’t get discouraged in the first 5 years if you don’t see your money growing dramatically yet

There’s a Chinese proverb that the best time to plant a tree was 20 years ago but the second best time is now

If you would like help to harness the power of compound interest schedule a time when we can discuss your particular situation.

Sources:

https://www.goodreads.com/quotes/76863-compound-interest-is-the-eighth-wonder-of-the-world-he

https://www.forbes.com/advisor/investing/average-stock-market-return/

“If you have any financial questions I would love to connect with you to help”

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.