529 to Roth IRA Conversions Under New Cares Act 2.0 Rules

Under the Cares Act 2.0 passed in December, savings from 529 education savings accounts can now be rolled over to a Roth IRA (starting in 2024).

This is an important update for parents or grandparents saving for their children or grandchildren’s future. A major concern with 529 accounts has always been “what if my child/grandchild doesn’t end up going to college”? Previously this would have triggered income tax and a 10% penalty to distribute that unused money. Under these new rules, the balance could now be rolled over to a Roth IRA for the beneficiary of the 529 (in this example the child/grandchild).

Under the Cares Act 2.0 passed in December, savings from 529 education savings accounts can now be rolled over to a Roth IRA (starting in 2024).

This is an important update for parents or grandparents saving for their children or grandchildren’s future. A major concern with 529 accounts has always been “what if my child/grandchild doesn’t end up going to college”? Previously this would have triggered income tax and a 10% penalty to distribute that unused money. Under these new rules, the balance could now be rolled over to a Roth IRA for the beneficiary of the 529 (in this example the child/grandchild).

This new rule creates a few major opportunities for savers:

You can take advantage of 529 account tax advantages to save for a child’s future education without as much concern you may be penalized in the future.

You could use a 529 as a “stealth Roth account” for a child to get savings growing tax-free for them long before they have an income that would allow you to fund an actual Roth IRA for them. An extra 15 to 20 years of compounding gains is a powerful thing!

In the “stealth Roth account” situation you may get the dual-benefit of state income tax deductibility as a bonus (this applies for states with income tax that allow a deduction for 529 contributions and assumes they won’t tax 529 conversions which is yet to be determined).

Open a 529 account for a child immediately and fund it with $1 or $25. This gets your 15 year conversion clock going (details on this below).

If your child received grants or scholarships that cover most of their costs they can be rewarded with a head start to their retirement savings by converting their 529 balance to a Roth IRA.

If you’re fortunate enough to be able to pay for your child or grandchild’s college out of pocket without using all of their 529 account, you could choose to transfer up to $35,000 to a Roth IRA for them instead of using it for college expenses.

Because this is the US Congress and tax code they couldn’t let it be toooo simple… there are some important rules to understand:

Funds must roll to a Roth IRA for the beneficiary of the 529 plan. If the 529 beneficiary is your child, that means it must roll to a Roth IRA for your child. Quick note - changing the beneficiary of a 529 is quite easy, congress and the IRS still need to clarify whether you could get around this provision by making you or your spouse the beneficiary of the account thereby allowing you to roll the 529 funds to a Roth IRA for you or your spouse.

Funds must be moved directly from the 529 plan to the Roth IRA, you can’t take the distribution as a check from a 529 and then separately go deposit to a Roth for the beneficiary.

The 529 plan must have been maintained for 15 years or longer before funds can be rolled over to a Roth IRA. Because of this requirement, I would strongly recommend most people open a 529 for a child when they are born and fund it with the minimum amount allowed (for example $1 or $25). This “starts the clock” toward the 15 year requirement in case you ever need to use this provision in the future.

The maximum amount that can be moved from a 529 plan to a Roth IRA during an individual’s lifetime is $35,000. This means you still don’t want to “overfund” a 529 account if you’re worried the beneficiary may not end up using the money for college.

Any contributions made in the past 5 years (and the earnings on those contributions) are not eligible to be moved to a Roth IRA. This doesn’t mean you can never move those funds, you just have to wait until they’ve been in the account for 5 years until you do.

Conversions from a 529 to a Roth IRA count toward the annual contribution limit for Roth IRAs ($6,500 for 2023). So only $6,500 could be converted in one year and no “regular” Roth contributions could be made if $6,500 was converted. If only $5,000 was converted during the year for example, the beneficiary could still make $1,500 in “regular” contributions for the year. This means to convert the full $35,000 lifetime limit would likely take 5 or more years.

Income limits do NOT apply for these conversions. Even if the beneficiary is over the income limit to make “regular” Roth IRA contributions, a 529 rollover to their Roth IRA would be allowed.

The beneficiary must have earned income equal to or greater than the converted amount. For example, if you want to convert $6,000 from a 529 to a child’s Roth IRA they must have at least $6,000 in earned income. If they only have $2,000 in earned income you can only convert $2,000. These are the same rules that apply for “regular” Roth contributions. Many kinds of income can qualify including summer jobs, babysitting, etc. If in doubt, consult a tax professional.

I know, that’s a lot of fine print and may be a bit confusing! I’d strongly suggest reaching out to an advisor if you think a 529 to Roth conversion may make sense for you or if you have questions about how this may impact you. I’m always available to answer questions by phone at 616.594.6205 and email at ryan@ffadvisor.com.

Inflation Is MUCH Lower Than You Think

The media and the average person misunderstand and misinterpret inflation for two important reasons:

They focus on the ANNUAL reported inflation number which tells you what has happened over the past year but not where inflation is headed.

The SHELTER component of inflation which measures rents and home prices makes up about one third of overall inflation but lags real-time housing data by up to 12 months.

The most recent inflation report that was published on 12/13/2022 makes an excellent illustration of these two points. Understanding the nuance of inflation reports and where we are headed rather than where we have been is key for setting expectations for how much further and how quickly the Fed will continue to raise interest rates as well as how long rates will remain elevated.

The media and the average person misunderstand and misinterpret inflation for two important reasons:

They focus on the ANNUAL reported inflation number which tells you what has happened over the past year but not where inflation is headed.

The SHELTER component of inflation which measures rents and home prices makes up about one third of overall inflation but lags real-time housing data by up to 12 months.

The most recent inflation report that was published on 12/13/2022 makes an excellent illustration of these two points. Understanding the nuance of inflation reports and where we are headed rather than where we have been is key for setting expectations for how much further and how quickly the Fed will continue to raise interest rates as well as how long rates will remain elevated.

Annual CPI (consumer price index) tells us how much prices have gone up over the past year as a whole.

This is the figure most often reported by the media. As shown in the line chart below, this figure peaked in June of 2022 at just over 9% and has been trending downward ever since to its current level of 7.1% (as of November 2022). This annual figure is calculated by taking all of the monthly increases for the past year (each of the bars in the bar chart below) and adding them together. For example, if you take all of the bars in the bar chart and add them together, you get that 7.1% current ANNUAL inflation.

This is great for telling us what happened over the past 12 months, but it’s a very bad way to measure what is happening right now. On the way up, the annual figure lags the real-time situation making it harder to see inflation heating up, and on the way down it lags the real-time situation making it hard to see inflation cooling down. Later we’ll see how the lag in rent and home price data makes this problem even worse.

A better way to understand what is happening right now is to ignore the ANNUAL number and instead ANNUALIZE the most recent 3-6 months of data. A couple of examples. If you take the most recent 6 months of data (June through November) you get a 4.5% annualized inflation rate. That’s much lower than the 7.1% figure for the past 12 months. If you take 5 months of inflation data (July through November) you get a 2.4% annual inflation rate. If you take the last 3 months of data you get a 3.6% annualized rate. These examples tell us that for the past 3 to 6 months we have been MUCH closer to the Feds official target of 2% annual inflation than most people believe.

It works the other way too - if you had taken the last four months of data when inflation peaked in June, you would have had an annualized inflation rate of 11.4%! This is much higher than the reported 9.1% annual figure.

Chart of annual cpi from bls cpi bulletin december 2022

chart of monthly cpi from bls cpi bulletin december 2022

Looking through this lens and understanding how annual inflation data lags what is happening right now shifts the narrative surrounding inflation. It didn’t just burst onto the scene a year ago and it hasn’t remained “stubbornly high” as the Fed has taken measures to push it back down to an acceptable range. According to the data, what actually happened was:

Inflation accelerated quickly as our economy reopened following the pandemic, particularly after the vaccine rollout in early 2021. The 3 month annualized rate (red line below) reached its first peak at 9.2% in June of 2021 while the annual rate that is broadly reported (blue line below) had just surpassed 5%. The Fed and many economists believed inflation would be transitory and inflation was not yet a “mainstream” topic.

Inflation remained elevated through it’s eventual peak in June 2022 but it wasn’t resisting the Fed’s efforts, the Fed just wasn’t doing anything. As the annual inflation rate caught up to the 3-month figure and gas prices spiked in January 2022, inflation became a hot mainstream topic (as evidenced by google search data).

As the Fed began to raise interest rates (yellow line below) in earnest with it’s first 0.75% increase in July 2022, the 3-month annualized inflation rate plunged into the range of 3% to 4% while the annual rate has lagged substantially in the 8% to 9% range. Ignoring this dramatic near-term decline and focusing on the much higher annual number would lead you to believe the Fed has “a lot of work left to do” when in reality the work may be nearly finished and the (lagged) data just hasn’t caught up yet.

chart was created using data from bls cpi bulletins dec 2018 - dec 2022, fed funds rate data from st louis fed

Home and rent prices accounts for a massive one third of CPI - but the way they are measured lags reality by UP TO 12 MONTHS

This is according to a paper written by the Bureau of Labor Statistics in conjunction with the Cleveland Federal Reserve Bank. An excerpt from their paper explains how large of an impact this has and why it’s such a big deal:

“Shelter is by far the largest component of the Consumer Price Index (CPI), accounting for 32 percent of the index. Accurate inflation measurement therefore depends critically on accurate rent inflation measurement, which is the primary input to both tenant and owner equivalent rent. It is therefore concerning that rent indices differ so greatly. For example, in 2022 q1 inflation rates in the Zillow Observed Rent Index (ZORI; see Clark (2020)) and the Marginal Rent Index (Ambrose et al. (2022)) reached an annualized 15 percent and 12 percent, respectively, while the official CPI for rent read 5.5 percent. If the Zillow reading were to replace the official rent measure in the CPI, then the 12- month headline May 2022 CPI reading of 8.6 percent would have read more than 3 percentage points higher.” (emphasis mine)

As the authors explain, if CPI had accurately reflected real-time data on home and rent prices, inflation would have peaked near 12%! Piling this huge lag for such a major component of CPI on top of a focus on the annual vs. near-term inflation rate puts policy makers and investors very out of sync with economic reality. Had the Fed paid more attention to the shorter-term trend and real-time data on rent and home prices sky-rocketing in the spring of 2021, they may have moved to raise interest rates 6 to 9 months sooner and curbed inflation at a rate of 5% to 6% rather than the near 10% rate we ultimately suffered.

This home and rent price lag is now working in reverse to create the illusion of higher inflation.

chart from st louis “Fred” website - data is published with a lag - sep 2022 most recent reported

Taking the principle above and applying it to our current situation, the rent & home price component of CPI today largely reflects the economic condition one year ago. At that time, the Fed had not even begun to increase rates and the average 30 year mortgage was around 3%. From June of 2021 through June of 2022, US home prices shot up by nearly 20% per the Case Schiller Index. That massive increase (which in reality happened in the past) will continue to feed through into CPI data making the rate of inflation look much higher than it really is. The reality is that From June 2022 through September 2022, home prices dropped by 2.6% or an annualized rate of 10.4% (September is the most recent data published by the Fed - the irony of this lag is not lost on me). So while home prices in reality are dropping, CPI data will continue to show robust price increases for its hugely important “shelter” component.

If you adjust the annualized 3-month inflation rate using CURRENT home price data, you see that inflation has slowed much more than official CPI data indicates.

If you replace the high growth rates the official CPI data use with zero growth in home prices over the past 3 months, the 3.6% annualized CPI rate we discussed earlier drops to just 0.85%. If you include the drop in home prices that the Case Schiller Index shows, the 3 month annualized rate of inflation drops even further to 0.2%! Both of these are well below the Fed’s target inflation rate of 2%.

Even if you strip out the recent price decreases for gas, energy, and used cars… without the lagged shelter component you’re still at just a 2.4% annualized inflation rate. All of this tells us that while some contributors to inflation like food, transportation, and some service industries may prove stickier and harder to bring back below 2%, if the current trend continues and no major geopolitical event occurs REAL inflation (ignoring that pesky lagged real estate component) is likely to remain in the 2% to 4% range.

The economists at the Fed aren’t stupid, they’re aware of the lag and impact of the real estate component. Heck, their own team wrote a paper on it! This should mean they factor it into their policy decisions and look through the noise in the data to the REAL economy. If they do, I’d expect the upcoming 0.5% increase to be the last large hike with the “final” rate topping out around 4.5%. Coincidentally, this is what the bond market is also predicting based on the current yield curve (12/13/2022).

MORE TO COME - I’ll be following this post shortly with another breaking down what this could mean for stock and bond markets in the coming year. In the meantime, I hope you enjoyed this trip down the rabbit hole of Inflation and CPI. Always remember, the media is a business. They are out for clicks and traffic, not to educate you. Scary headlines and political narrative sell. I encourage everyone to seek out the data and let it speak for itself or rely on trusted advisors who do the digging for you.

Footnotes

All CPI data is from official Bureau of Labor Statistics bulletins

Case Schiller home price data and Fed funds rate data is from the St. Louis Federal Reserve website

My own calculations of annualized data modified by adding/removing/adjusting specific components is based on archived CPI bulletins published by the Bureau of Labor Statistics from 2018 through November 2022.

Current 3-month and 6-month annualized calculations were based on the November 2022 bulletin detailed categories data from the BLS.

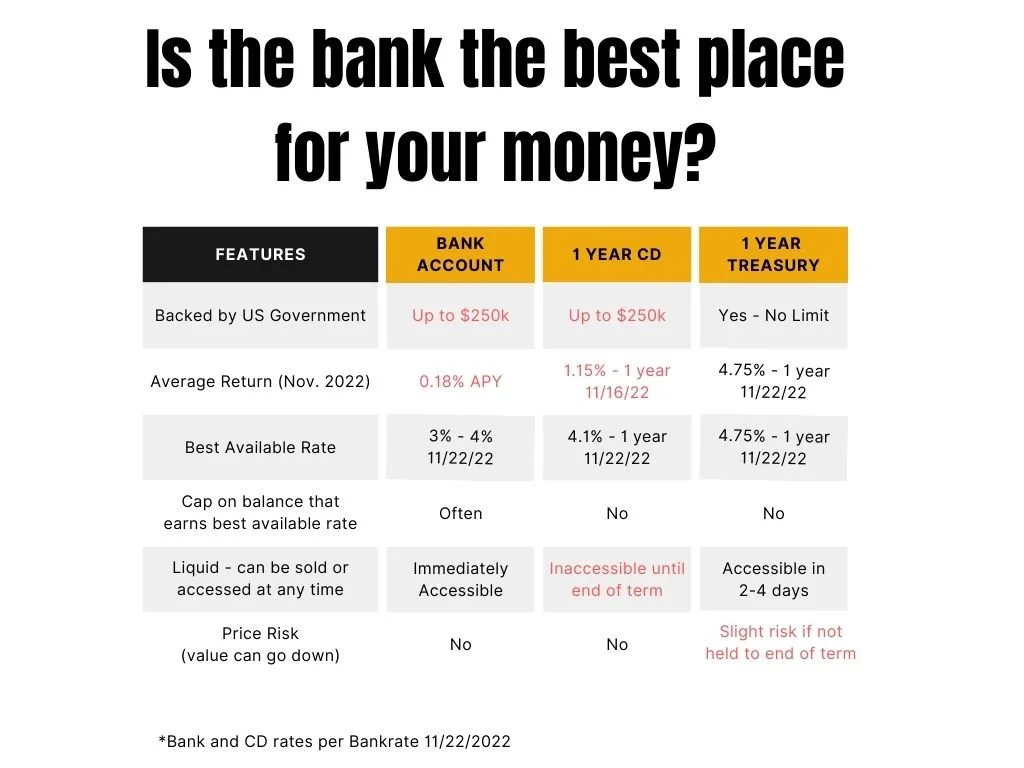

Why Is Your Cash In The Bank?

Typically, people keep money in the bank for three reasons: 1. Safety 2. Return (interest) 3. Accessibility. In the current environment, short-term bonds actually beat banks on two of those three criteria and aren’t far off on the third.

NET OUT - If you’re willing to hold a treasury bond until the end of it’s term, you know the minimum return you will receive, the only risk of loss is if the US government defaults on its debt, and your bond has the potential to do better than expected if interest rates drop.

Why is your cash in the bank? This question may sound absurd… where else would it go? Under my mattress? The truth is, few people understand bank deposits and bonds well enough to know that they have other options, and those options may actually (at the moment) be much better.

Typically, people keep money in the bank for three reasons: safety, return (interest), and accessibility. In the current environment, bonds actually beat banks on two of those three criteria and aren’t far off on the third.

SAFETY - Treasuries are even safer from default than bank accounts.

This is especially true if you have a large amount of cash. Don’t get me wrong, FDIC insured banks are a very safe place to keep your money. The FDIC automatically insures up to $250,000 per depositor with the full faith and credit of the United States government. However, above that limit, cash is only secured by the faith and credit of the bank institution itself.

In contrast, every treasury bond is backed by the full faith and credit of the US government with no limit.

What about all that debt our government is racking up, how can I trust that they won’t default? I won’t get into this argument other than to say that the US government is almost universally considered to be the least likely institution in the world to default. Further, if you don’t trust the US government to pay their debts, you shouldn’t trust FDIC insurance either. Remember, FDIC Insurance is just a promise by the government to pay depositors (up to $250k) if the bank fails to do so.

The net out is that for the first $250,000, banks and treasury bonds have essentially the same risk of default and above $250,000, treasury bonds have less risk of default.

RETURN - Bonds (finally) offer a decent return while interest paid by many banks has hardly increased.

As of 11/10/2022, the average savings account yielded 0.18% APY (per bankrate). Fortunately some banks pay a higher rate up to 3% or 4% but typically the amount allowed to earn this higher rate is limited to $10,000 or $15,000. These can also come with obnoxious requirements to have enough direct deposits or debit card purchases. CD’s are better, yielding on average 1.15% with the best available rate at 4.1% per bankrate.

In contrast, as of 11/22/2022, 1-month treasuries yielded 3.97% and 1-year treasuries yielded 4.75% (per treasury.gov). Unlike many high interest bank accounts, there is no limit on how much you could invest at those rates and no special rules or hoops to jump through.

ACCESSIBILITY - Bonds can be sold and converted to cash in a matter of days.

It’s hard to beat a bank account for convenient storage and access of your cash. That’s what modern checking and savings accounts are for. However, this convenience and accessibility comes at a price. Because you can demand your cash from the bank at any time, they must keep a large amount of money in reserve. They can’t lend or invest those reserves which means they can’t generate profit from them. This is at least part of the reason banks offer pretty stingy rates on your accounts or cap the amount that can receive a high interest rate (think LMCU or Consumers Credit Union).

CD’s take a different approach. You promise the bank you won’t touch your money for several months or years and, because they know when you will receive your money back, they can use your deposit to lend, invest, and otherwise make money. In return, they pay you a higher rate. The major drawback is the contract you make not to touch your money until the term is up. Your money is essentially locked up so you better know you won’t need it until the agreed-upon date.

This is where short term Treasuries at today’s rates shine. There is a large and highly liquid market for US treasuries, meaning they can easily and quickly be sold and turned into cash if needed. This process should take only a few days. So, not only do short term treasuries currently have a higher return than CD’s, they’re a much better investment if you may want or need your money within the next few months or years. Some typical situations that require this are cash set aside for a home purchase or business investment, for a future tax bill, or to generate some return while buying into the stock market over time (dollar-cost-averaging).

The value of your bonds can go down if they’re not held until the end of their term.

This is a major difference from bank accounts or CD’s where the value of your account doesn’t fluctuate based on markets or interest rates. When interest rates rise quickly as they have this year, bond prices drop. This is because new bonds being issued as rates continue to rise pay a higher rate than bonds issued 3 months, 6 months, or 1 year ago. Naturally, if you want to sell your old bond that’s paying a lower rate than bonds issued today, buyers demand to buy them at a discount so that their total return if they hold the bond until the end of its term is the same as a bond purchased today.

Here’s the good news, this risk of your bond dropping in value only exists if you sell it before the end of its term. If you hold your bond until it matures you know exactly what your return will be because the US government will pay you its initial value plus your interest. This is one reason holding actual bonds can be preferable to bond mutual funds or etfs. Bonds are more complex to buy and sell but you can lock in specific terms, return rate, and you are in control of if and when to sell a bond or hold it to maturity.

Some more good news, short-term bonds for 1 month, 3 months, or 6 months change much less dramatically in response to interest rates than longer term bonds like 10-year or 30-year treasuries. AND, to top it off, short term bonds are currently paying higher rates of return than long-term bonds (thanks to an inverted yield curve which is a somewhat rare phenomenon and a topic for another time).

Lastly, this price movement can also work for your benefit. If interest rates drop, the value of your bonds will increase meaning you could sell them prior to maturity for a better return than you expected. The net out is that if you’re willing to hold a treasury bond until the end of it’s term - you know the minimum return you will receive, the only risk of loss is if the US government defaults on its debt, and your bond has the potential to do better than expected if interest rates drop.

Don’t just throw away your investments and strategy to go buy short-term bonds!

Yes short-term bonds are currently a great option FOR A SPECIFIC PURPOSE. If you’re looking for a place to safely park cash that you may need in the next few months or years and make a decent return… short-term bonds sure seem to beat the bank. If you’re saving for a far-off goal, 4% to 5% return likely isn’t the best you can do. Over long periods of time, stocks and long-term bonds have historically outperformed short-term bonds. If you have a strategy, stick to it. If you’d like a strategy, please reach out. You can reach me by email at ryan@ffadvisor.com or cel phone: 616.594.6205.

Footnotes

Bank & CD Rates per bankrate on 11/22/2022

Bond rates per Daily Treasury Par Yield Curve Rates on treasury.gov - 11/22/2022

Mega-Backdoor Roths Aren't Just For "Rich" People

There are many examples of situations where mega-backdoor roth contributions can be unexpectedly relevant but there are some overarching themes:

When the amount of money coming in during a year is significantly higher than usual

When your expenses are significantly lower than usual but your income hasn’t changed

When you’ve built up more savings than you need for your emergency fund and short-term goals

When one spouse has access to a 401k and the other working spouse does not

When many people learn about mega-backdoor Roth 401k contributions, they think to themselves, “this sounds like a great strategy for “rich” people”. Sure, it can be a lot easier for someone with a very high income to afford a $60,000 or $70,000 contribution every year and high earners are definitely a group that can benefit hugely from the mega-backdoor. But, there are two things I’d like to point out:

A lot of income doesn’t necessarily translate into a lot of disposable income or savings. Without the right money habits, people tend to spend more as they earn more and can even end up feeling like they have less of a cushion than they did when they earned less.

Income is just one part of a larger financial picture. Too many people never think beyond income and their basic 401k contribution to consider ways their savings, assets, debt, and expenses interact with and can complement those basic building blocks.

You could write an entire book on point #1 but I want to focus on point #2 with five examples of relatively common situations where, when you look at the whole picture, mega-backdoor contributions are attainable and can make a lot of sense, at least in a given year or time period. If you don’t have a clear idea of what your “whole financial picture” looks like, please reach out, that’s exactly what I’m here for.

You have a self-employed spouse. While there are several retirement account types available to self-employed individuals (we set these up often for new clients), many people either aren’t aware of them or feel it will be too complicated to set them up. In this situation it makes sense to think about your combined income and turn the spouse who does have access to a 401k into the super-saver of the family. If one spouse has no account to save for retirement, it can be pretty feasible for the other to be able to max out their 401k contribution and then use the mega-backdoor to boost savings even further.

You have extra cash after selling a home. With the massive increase in home prices some people are finding they’ve accumulated enough equity to have cash left over, even after making their down payment on a new home. Often people are unsure what to do with this cash and will let it sit in the bank earning nothing. Some may at least take the step of investing it so it can grow. But, that growth will be taxed. In this situation, maxing out a 401k and then making a mega-backdoor roth contribution is an ideal way to essentially shift that money into a tax-free account where it can grow and never be taxed again!

You have more in the bank than you need for your emergency fund. This could be a sign that you’ve been under-saving for retirement. If so, maxing out your 401k for a year or two and making extra mega-backdoor contributions is a great way to catch up, get that money growing, and avoid tax on that growth. If you have been saving enough and are still in this boat, layering on mega-backdoor contributions could help get you to retirement or financial independence sooner than you thought possible.

You had a windfall or unusually high compensation this year. Most people don’t win the lottery so more often this could be an inheritance, a gift from a family member, an unusually large bonus at work, a stock grant, or an unusually “good year” for commission-compensated workers. Often in these situations the income is unexpected and therefore not already “spoken for”. If you want to avoid the temptation of spending it just because it’s there, a mega-backdoor contribution is a great way to essentially shift this money to an account where it can grow tax-free.

You moved or made a life change that has reduced your expenses dramatically. As remote work exploded during the pandemic, some people have been able to keep jobs with “big city” or “coastal” pay while moving to areas of the country with a much lower cost of living. Others may have moved in with aging parents to help care for them and have seen their living costs plummet as a result. Maybe kids moved out or finished college that you were paying for. While maxing out your 401k may have been unobtainable before, it may now be a very real option to consider along with going even further and making mega-backdoor contributions.

There are many more examples of situations where mega-backdoor roth contributions can be unexpectedly relevant but there are some overarching themes:

When the amount of money coming in during a year is significantly higher than usual.

When your expenses are significantly lower than usual but your income hasn’t changed.

When you’ve built up more savings than you need for your emergency fund and short-term goals.

When one spouse has access to a 401k and the other working spouse does not.

If you need a primer on what a mega-backdoor roth contribution is and how to make one you can check out my summary blog post on this topic: Mega-Backdoor-Roth

2023 Contribution Limit and Tax Adjustments (mostly) Keep Up with Inflation

While the 2023 social security cost-of-living increase of 8.7% grabbed most of the headlines, the IRS also adjusted tax brackets and contribution limits for 2023 to keep pace with the 8.2% annual inflation rate reported in October. While many adjustments kept up (401k contribution limits increased 9.8%, IRA limits by 8.3%), the Feds were stingier with others (tax bracket thresholds increased only 7.1%, the standard family deduction by 6.9%, Roth income limit by 6.9%).

While the 2023 social security cost-of-living increase of 8.7% grabbed most of the headlines, the IRS also adjusted tax brackets and contribution limits for 2023 to keep pace with the 8.2% annual inflation rate reported in October. While many adjustments kept up (401k contribution limits increased 9.8%, IRA limits by 8.3%), the Feds were stingier with others (tax bracket thresholds increased only 7.1%, the standard family deduction by 6.9%, Roth income limit by 6.9%). I’ve summarized the major updates for 2023 below.

If you have any questions about how these changes may impact your saving or financial plan in the coming year feel free to reach out to me at ryan@ffadvisor.com or 616.594.6205.

Retirement Account Updates

401k contribution limit increased by $2,000 from $20,500 to $22,500

IRA contribution limit increased from $6,000 to $6,500

401k catch-up contributions increased from $6,500 to $7,500

IRA catch up contributions did not increase, they are still $1,000

SIMPLE retirement account contribution limit increased from $14,000 to $15,500

Roth IRA income limit phase-out increased:

Between $138,000 and $153,000 for singles and heads of household

Between $218,000 and $228,000 for married filing jointly

SEP IRA contribution limit increased from $61,000 to $66,000

HSA contribution limit increased from $3,650 to $3,850 for singles. Family coverage increased from $7,300 to $7,750.

Tax Updates

Standard Deduction for 2023: Married filing jointly $27,700 up $1,800 from the prior year. For single taxpayers and married individuals filing separately, the standard deduction rises to $13,850 for 2023, up $900.

Tax Bracket Adjustments for 2023:

35% for incomes over $231,250 ($462,500 for married couples filing jointly);

32% for incomes over $182,100 ($364,200 for married couples filing jointly);

24% for incomes over $95,375 ($190,750 for married couples filing jointly);

22% for incomes over $44,725 ($89,450 for married couples filing jointly);

12% for incomes over $11,000 ($22,000 for married couples filing jointly).

For tax year 2023, the foreign earned income exclusion is $120,000 up from $112,000 for tax year 2022.

Estates of decedents who die during 2023 have a basic exclusion amount of $12,920,000, up from a total of $12,060,000 for estates of decedents who died in 2022.

The annual exclusion for gifts increases to $17,000 for calendar year 2023, up from $16,000 for calendar year 2022.

Social Security Updates

COLA Increase for 2023 will be 8.7%

Earnings limit for social security benefit adjustment for workers younger than full retirement age: $21,240

Fiduciary Financial is not a tax advisor, these figures are provided for informational purposes only.

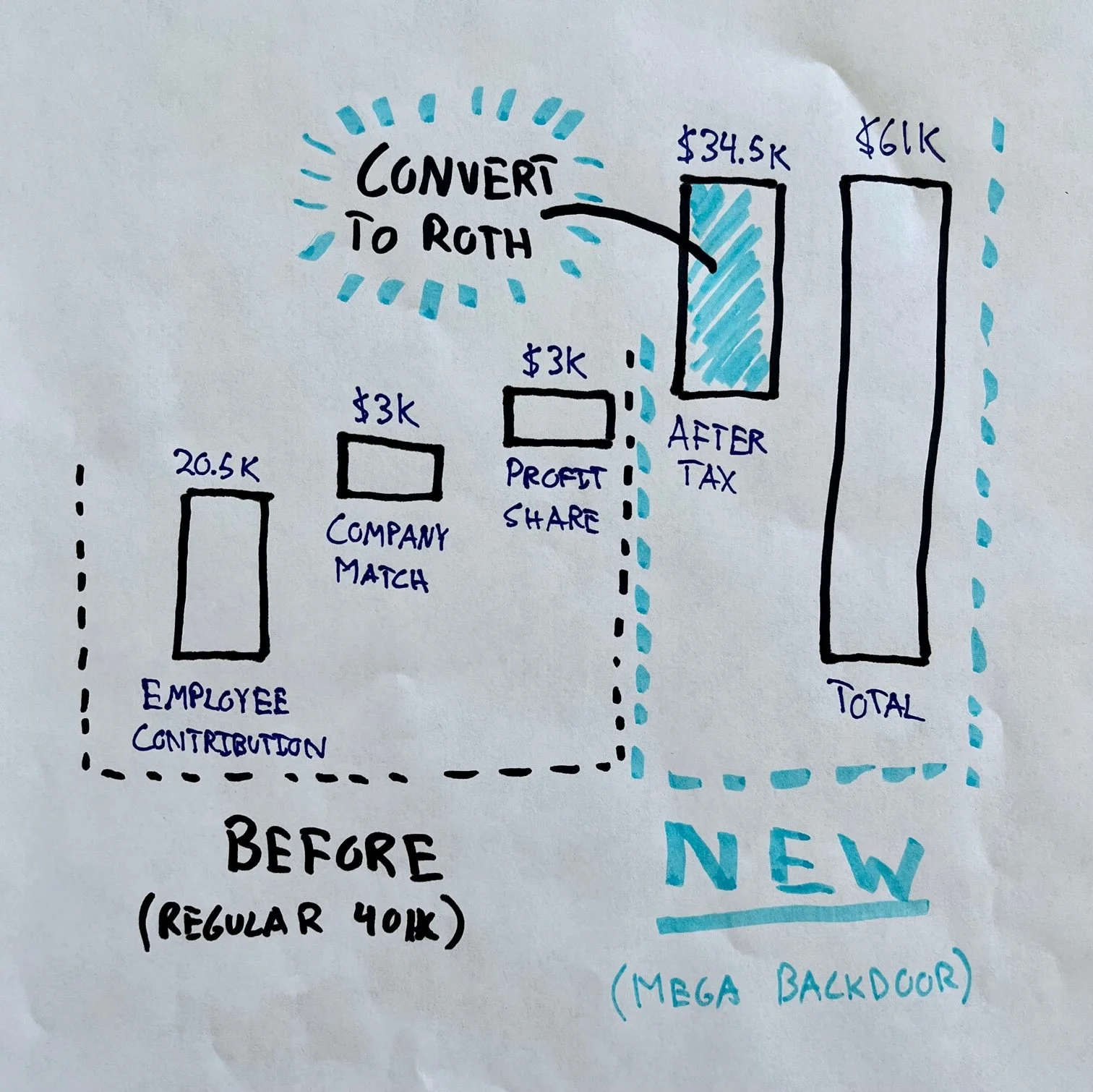

Mega-Backdoor Roth - The Hidden 401k Feature that can Supercharge Your Retirement Saving

Saying that the Mega-Backdoor Roth strategy can supercharge your retirement saving is not a hyperbole. In most situations, maximizing this feature MORE THAN DOUBLES the amount you can save to Roth accounts each year. Once those savings are invested in a Roth account, they can grow tax free for years or decades and be withdrawn tax free* in retirement.

The “mega-backdoor” can have mega tax impacts

A quick example illustrates just how powerful those tax savings can be:

Each year for 20 years, “normal 401k Charlie” maxes out his Roth 401k with $20,500 and invests an additional $40,500 in a taxable investment account. Both accounts grow at 6% per year. At the end of 20 years, Charlie has $1,497,169 in his taxable account and $757,826 in his 401k; $2,254,995 in total. While Charlie’s Roth 401k savings can be withdrawn tax free in retirement, he will owe capital gains tax on the $687,169 of his investment gains in the taxable account. At long term capital gains rate of 15% that would be $103,075 in taxes! This doesn’t even include taxes he would likely have paid on dividends in the taxable account over 20 years.

“Mega-backdoor Bettie” on the other hand maxes out her normal $20,500 Roth 401k contribution and is able to invest an additional $40,500 into her Roth 401k through the Mega-backdoor strategy. After 20 years, with the same investment return as Charlie, Bettie has the same total savings of $2,254,995. However, Bettie can withdraw that full amount tax free in retirement.

In this example the Mega-backdoor saved Bettie $103,075 on taxes! She also didn’t pay tax on any dividends along the way.

How to implement the Mega-Backdoor strategy

Hopefully this example helps illustrate that the Mega-Backdoor Roth can be a powerful tax-saving strategy, but how does it work? By making after-tax 401k contributions and in-plan Roth conversions. Let’s break those two steps down:

1) Allowing after tax 401k contributions increases the maximum amount employees can contribute from $20,500 in 2022 to $61,000* (or $67,500* if you’re over 50). After-tax contributions don’t reduce your taxable income or tax bill today, but this is where the in-plan Roth conversion is key.

2) Through an in-plan conversion you can easily take those huge after-tax contributions and convert them to Roth funds within your 401k (or through rollover conversions to a Roth IRA). Once converted, your savings grow tax-free and can be withdrawn tax free in retirement just like normal Roth 401k or Roth IRA contributions.

This is the power of the mega-backdoor, it allows you to quickly build a much bigger tax-free* retirement nest egg than you could with a typical 401k and Roth IRA alone. And, unlike a Roth IRA where households over the income limit aren’t allowed to contribute, anyone in the plan can contribute with no income cap. This means even high earning households can mega-backdoor. It’s actually this group that can benefit the most!

Some 401k plans don’t support the Mega Backdoor and some require an extra step

Unfortunately, many 401k plans don’t allow allow for employees to make after tax contributions. Sadly, there’s not even a good reason for this other than perhaps some added administrative difficulty. That said, it is becoming more and more common and will likely continue to grow in popularity. Some plans allow for after tax contributions but don’t have a program set up for in-plan conversions to Roth. This is where a second step is needed to see if the plan does allow for “in service distributions” so that employees can roll over their after tax contributions to an IRA and convert them to Roth. If you’re unsure what you’re plan allows or how to execute this step please reach out, I’m happy to help.

The Mega Backdoor isn’t right for everyone

Let’s be honest, making mega-backdoor Roth contributions isn’t realistic for a lot of people. Maxing out a $20,500 annual contribution is already a lot! In fact, it may already be more than enough for your situation and retirement goals. That said, there are a lot of unique situations where a mega backdoor strategy can become unexpectedly relevant, I’ve written about several of them here: Mega-Backdoor Roths Aren’t Just for Rich People.

Like any large money decision, mega-backdoor Roth contributions should be part of a bigger financial and tax strategy built around your needs, your timeline, and your goals. If you’d like help building a strategy tailored to your timeline and goals (or figuring out if your employer allows the mega-backdoor), feel free to reach out, I’d love to see if I can help or direct you to someone who can. You can reach me by email at ryan@ffadvisor.com or cel phone: 616.594.6205.

Footnotes:

*Roth savings grow tax-free. Contributions can be withdrawn without tax or penalty at any time and investment gains can be withdrawn tax and penalty-free after age 59-½ (or 55 if the “rule of 55” applies to you).

*$61,000 and $67,500 are the 2022 limits for employee contributions, employer matches, and profit sharing contributions combined. Your max contribution = $61,000 or $67,500 - employer match - profit sharing contribution.