If you’ve ever felt that the world of investing is confusing and intimidating, you’re not alone. There is a lot of information, but it can be a challenge to know where to start. Let’s explore the steps necessary to begin investing, simplify your approach, and figure out what is going to work for you.

Investor Types

There are three main types of investors. The first is someone who prefers to be hands-off and hires an advisor to manage their entire financial picture, like a personal CFO. The second person likes to take the DIY approach to financial management. The third individual falls somewhere in between, opting to hire a financial advisor for their investment management while staying informed on the strategy and approach being used. Each of these approaches has its pros and cons, but it is important to know that all can be effective at different times.

Establish an Emergency Fund

Regardless of your approach, before you start investing, it is wise to establish an emergency fund that will protect you and your family in case of… well, an emergency! Having this fund in place will allow you to start investing and stay consistent, even if you have major expenses arise. Once your emergency fund is established, you can sort out the remaining information needed to begin investing.

Goals and Risk

The first step to investing is to understand your individual goals and risk tolerance. This is entirely custom to your financial situation, so it is important to not take a blanket approach. Examples of financial goals might include saving for your child’s college education, retirement planning, or vacation. Each of these goals will come with its own timeline and risk tolerance. It is important to select accounts that will line up with your savings goals. For instance, if you are saving for a college education, you might choose to invest in a 529 plan since it is an education-specific account.

Once the account is established, you can determine the timeline of your investment, and what risk you are willing to absorb. You will often see longer investments placed into a more aggressive allocation because you have more time to absorb the fluctuations of the stock market. If your timeline is short, however, you may prefer to use a more conservative investment approach. It is important to continually adjust your risk tolerance over time, and if you are not confident in your ability to manage this, don’t hesitate to seek out a professional.

Investment Capacity

In this example, we will assume that you are already contributing to an employer plan to get the employee match, which can often be a great starting point for investing. Beyond that, you have to decide how much money you are willing to invest consistently, based on your current budget. I discuss this in my post, “Mastering Your Money: Budgeting Essentials and When You Need Them”. I am a fan of incorporating investment contributions into your monthly budget if possible, and automating those contributions. This eliminates the concern of “timing the market” and allows you to take advantage of time in the market.

Pick a Strategy

Now that you have your emergency fund, established goals, risk tolerance, and your investment capacity, you can now decide on your approach to investing. For the DIY investor, it is important to do your research and find a strategy that has historically performed consistently well. This is not the time to dump all your money into the newest investing “fad”. Find a good balance of investments that aligns with your goals and risk tolerance. The balance that you want to see here is called diversification. This means that you are intentional in picking funds that give you broad exposure to the stock market, as opposed to putting all of your eggs in one basket.

If the thought of picking investments, or even doing the research is intimidating, it might be time to seek out a certified investment advisor who can help guide you through everything I’ve outlined here. When doing so, make sure to find a fiduciary advisor who is not going to make commissions on your investment selection.

Stay the Course

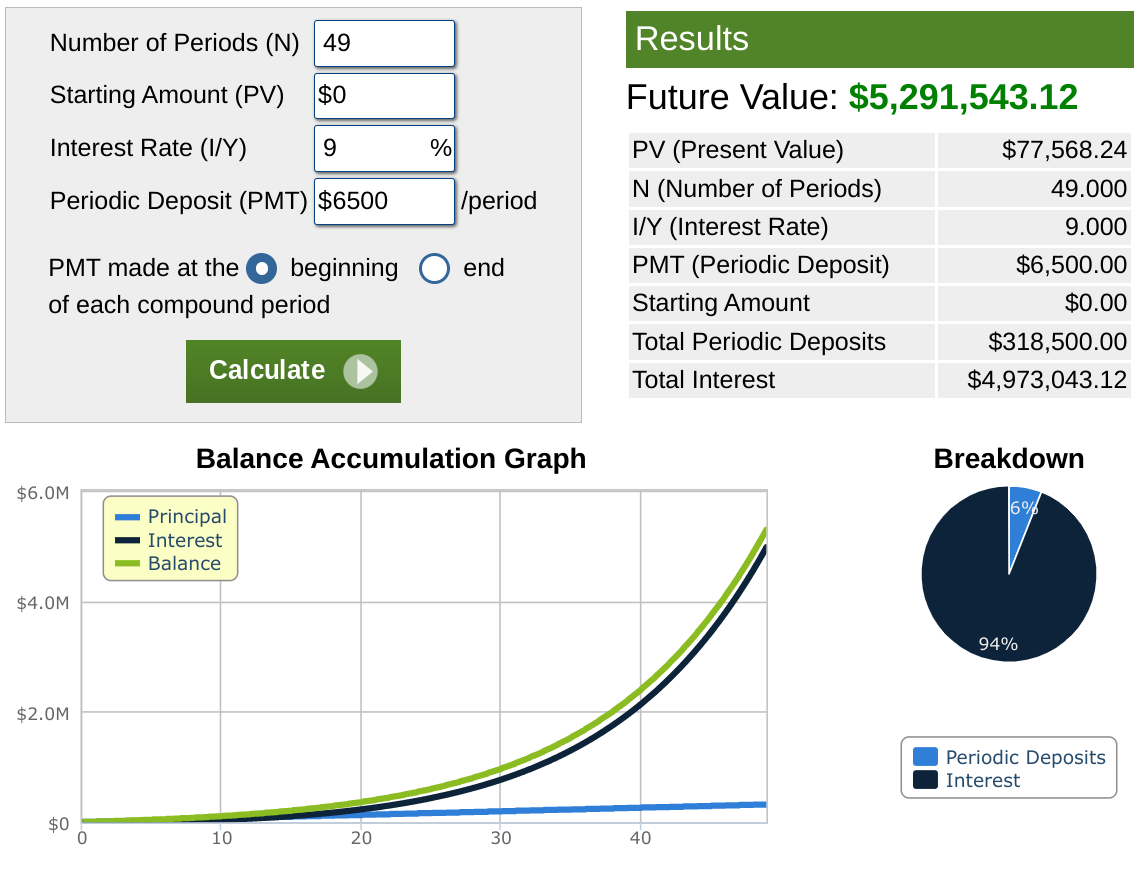

The final piece, and perhaps the most important is to stay the course. Investing is a long-term play that will have fluctuations over time. Some people handle this fluctuation better than others. If you struggle with the fluidity of the market, try not to view investments on a weekly or monthly basis, but on a yearly basis or longer. As we saw in the graph above, avoiding the market is not the answer.

Keep in mind that there is no one-size-fits-all approach to investing, and what worked for someone may not be what is best for you. Have confidence in your approach, and stay the course.