Making the Most of Cash Balance Plans: A Simple Guide for Business Owners

If you own a business and want to save more for retirement while paying less in taxes, a cash balance plan might be a great option. These plans may allow you to save more money than a regular 401(k) and offer major tax benefits.

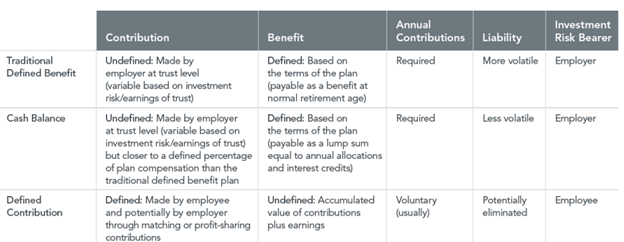

What is a Cash Balance Plan?

A cash balance plan is a type of employer-sponsored retirement plan where the business makes annual contributions on behalf of employees. These contributions grow at a predetermined rate and are designed to provide a stable retirement benefit. Unlike traditional 401(k) plans, where employees contribute and take on investment risk, a cash balance plan ensures the employer funds the account and assumes the investment risk.

Key Benefits of Cash Balance Plans

1. Higher Contribution Limits

A 401(k) has limits on how much you can put in; $70,000 per year ($77,500 if you're 50 or older) for 2025. A cash balance plan lets you save significantly more, sometimes exceeding $300,000 per year, depending on age and income. This is especially helpful for business owners who want to accelerate their retirement savings and take advantage of tax-deferred growth.

Source: Joe Nichols, DWC - The 401(k) Experts.

2. Substantial Tax Savings

Source: Joe Nichols, DWC - The 401(k) Experts.

Contributions to a cash balance plan are tax-deductible, directly reducing taxable income. This is particularly valuable for high-income business owners looking to lower their annual tax bill. Additionally, the plan's assets grow tax-deferred, allowing for compounding benefits over time.

This video is an audible version of this article. Feel free to listen while reading, or watch it independently.

3. Enhanced Employee Retention and Satisfaction

Offering a strong retirement plan helps businesses attract and retain skilled employees. A cash balance plan provides a predictable benefit, making it an appealing option for employees seeking long-term financial security. Business owners who offer these plans often find that they increase employee loyalty and job satisfaction.

4. Flexibility in Plan Design

Cash balance plans can be customized to meet the needs of the business. Contributions can vary based on employee roles, tenure, or salary levels, allowing business owners to structure the plan in a way that best serves their financial and workforce goals. Additionally, these plans can be paired with a 401(k) for even greater retirement savings potential.

Challenges of Cash Balance Plans

1. Required Annual Contributions

Unlike profit-sharing contributions in a 401(k), which can be discretionary, cash balance plans require mandatory annual contributions. This means businesses need a consistent and predictable cash flow to maintain the plan over time.

2. Administrative Complexity

Cash balance plans involve more administrative work than traditional 401(k)s. Business owners must comply with government regulations, complete annual actuarial evaluations, and file IRS reports. Engaging a third-party administrator (TPA) is necessary to ensure compliance and smooth plan operation.

3. Funding Requirements

Since the employer is responsible for funding the plan and ensuring returns meet the guaranteed rate, market downturns could lead to additional funding obligations. For example; a plan with $1 million of accumulated benefits could experience an investment shortfall of 5% based on market performance. This would require an additional $50,000 of employer contributions on top of the annual contribution requirements. It should be noted that any losses may be amortized over a 15-year period.

Source: Joe Nichols, DWC - The 401(k) Experts.

4. Higher Setup and Maintenance Costs

Compared to 401(k) plans, cash balance plans typically have higher setup and maintenance costs. Employers must factor in administrative fees, actuarial costs, and investment management expenses when determining if the plan is a viable option.

Is a Cash Balance Plan Right for Your Business?

A cash balance plan is a powerful tool for business owners who want to accelerate retirement savings and take advantage of significant tax breaks. While these plans require mandatory contributions, careful planning can ensure long-term benefits that often outweigh the administrative and funding challenges. For high-earning business owners with a steady cash flow, a cash balance plan can provide a strategic way to maximize retirement savings while significantly reducing taxable income.

These plans are particularly beneficial for professionals such as doctors, lawyers, and consultants who have stable profits and seek to invest heavily in their future. By assessing your financial stability and working with experts, you can determine if a cash balance plan aligns with your long-term business and retirement goals while also offering valuable benefits to your employees.

Recent Articles Written By Andrew:

Recent Publications Featuring Andrew:

Podcasts Featuring Andrew:

Fiduciary Financial Advisors, LLC is a registered investment adviser and does not give legal or tax advice. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. The information contained herein has been obtained from a third-party source which is believed to be reliable but is subject to correction for error. Investments involve risk and are not guaranteed. Past performance is not a guarantee or representation of future results.

Fiduciary Financial Advisors does not give legal or tax advice. The information contained does not constitute a solicitation or offer to buy or sell any security and does not purport to be a complete statement of all material facts relating to the strategies and services mentioned.

When couples combine finances, the real challenges are rarely about math. They're about autonomy, fairness, and trust. This guide walks through four approaches to merging money (from fully separate to fully joint), explains how financial needs shift across life stages, and outlines the legal risks of changing asset titling without professional counsel. Written for high-earning professionals navigating income disparity, career transitions, and the emotional weight of financial intimacy.